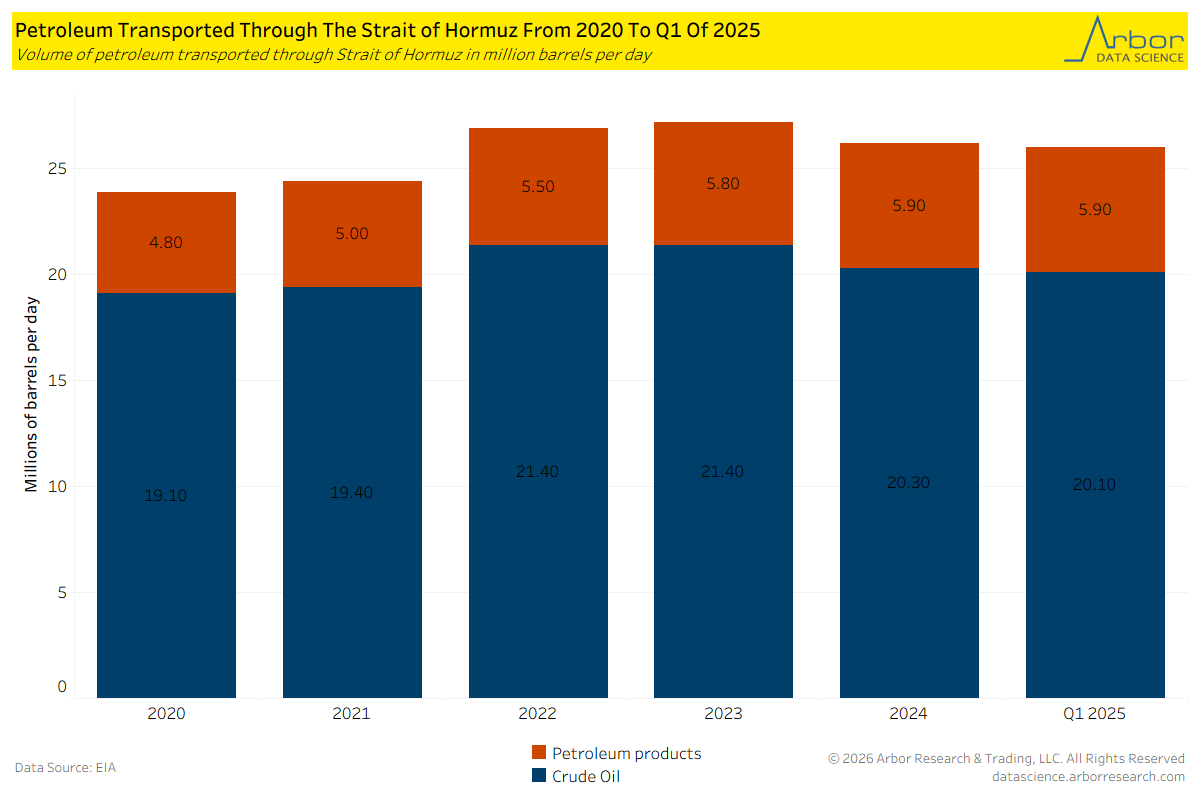

With the Middle East currently in an all out war, it is a good time to take a step back and look at what this means for the world’s energy markets. Of course, there are the two major (likely to be recurring) headlines that are and will dominate – Iran energy supply (mostly to China) and the Strait of Hormuz. Iran is a decent size player in the oil game with a few million (give or take) barrels daily going to friendly states. But, it is importantly positioned on the Strait of Hormuz, the primary choke point in getting energy from much of the Middle East to the rest of the world.

Importantly, Iran does not currently really have the ability to effectively close the Strait. Maybe it did. But it does not at the moment. Much of the Iranian Navy is no longer operational, and it will be difficult for the Iranian military to concentrate on the Strait during the current bombardment. Not to mention, many of Iran’s neighboring countries are no longer friendly following Iran targeting them. That makes closing the Strait exceedingly difficult.

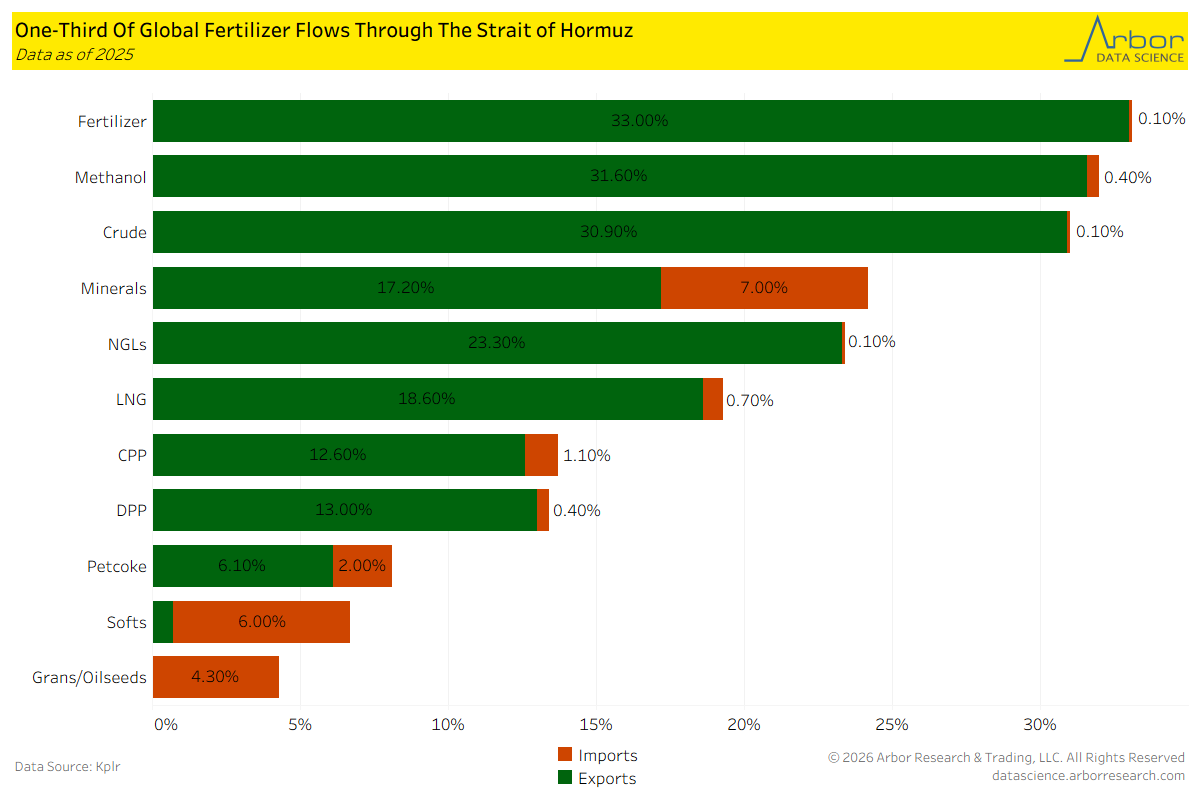

But, it is not simply oil. There are also the derivatives that surround the energy complex. One of the major ones is fertilizer and another is LNG. That is potentially problematic going into the planting season in the Northern hemisphere as farmers cannot “wait out” a price spike to plant crops. Luckily for Europe (which is highly reliant on LNG for Qatar and other Gulf States), the heating season is coming to an end.

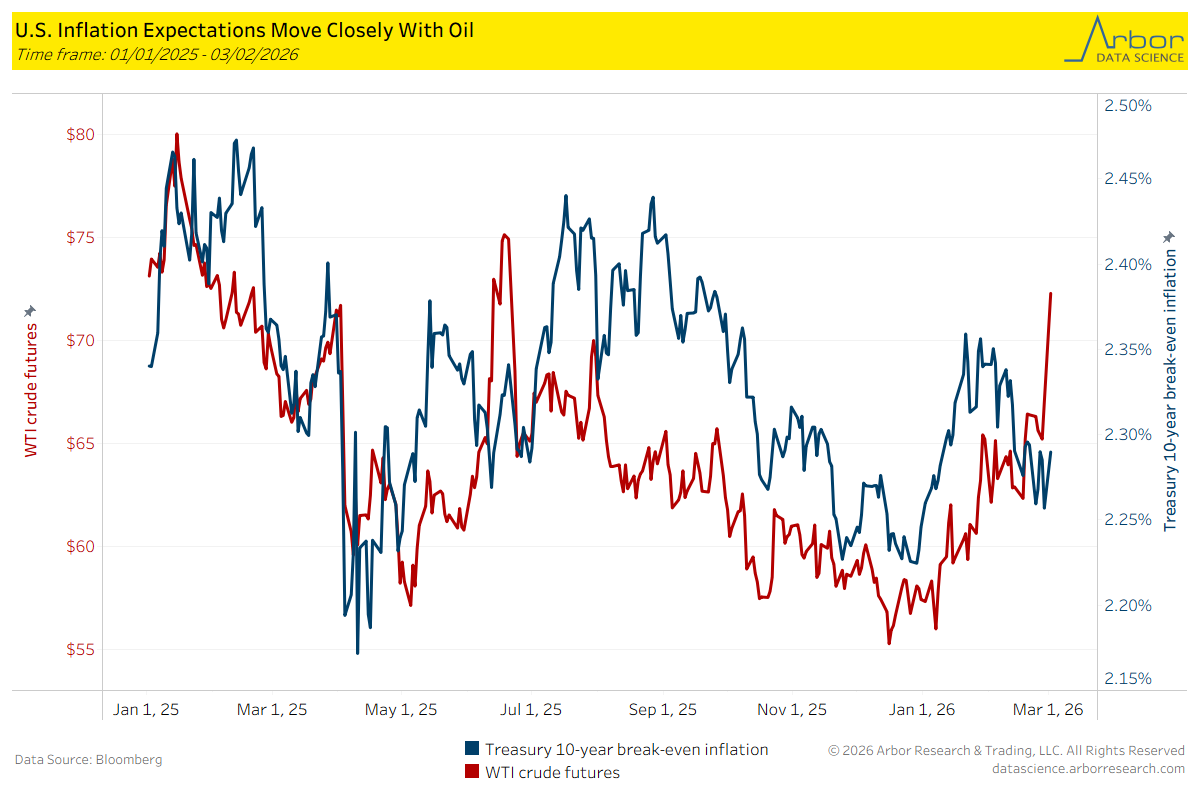

The current moderate spike in energy prices is likely to push longer end yields higher. But not too much. Why? Frankly, the spike in energy prices is not all significant (outside European gas prices). That should keep the reaction in yields at least moderately contained.

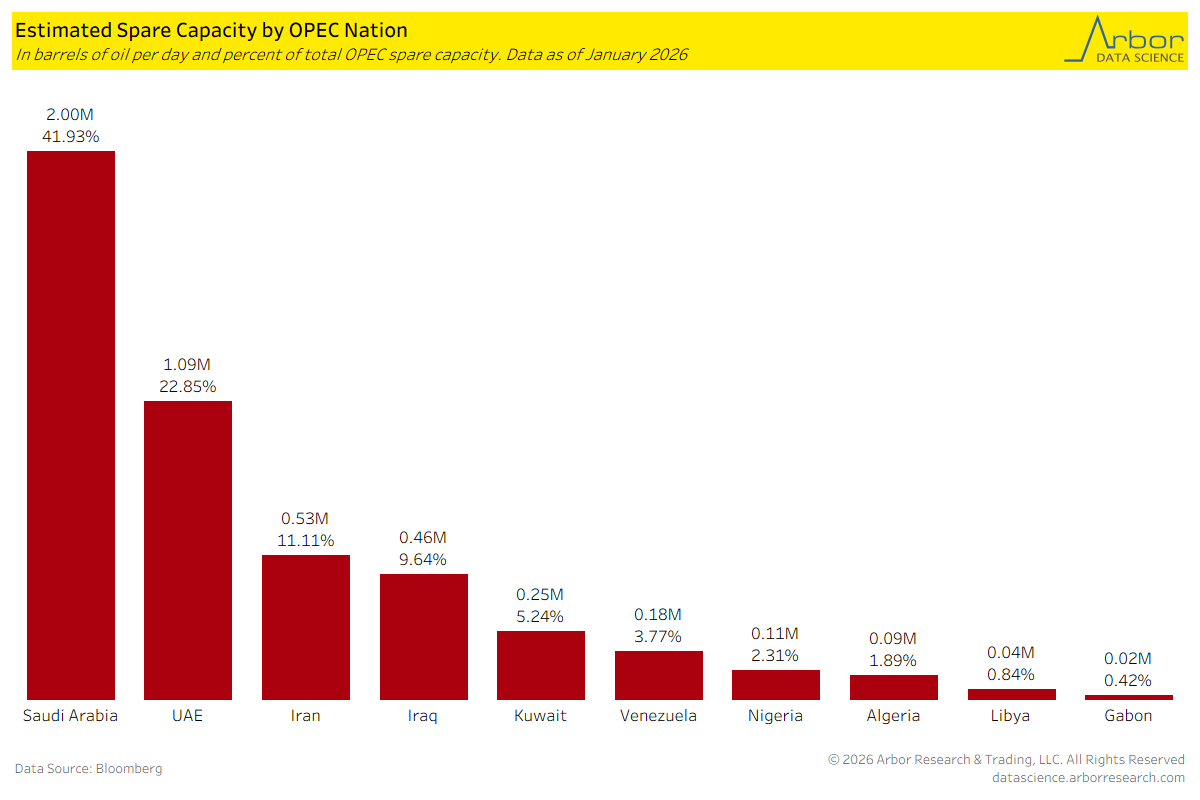

Not to mention, there is plenty of spare capacity (assuming it does not get attacked) outside of Iran. And that is something that should not be overlooked. It is not as though the world was in an oil supply crunch going into the current conflict. It was closer to a glut. That is part of the reason oil is struggling to move much higher. At roughly $70, it is far from prohibitively expensive.

While Iran is important for energy markets, the security of its neighbors is far more important. As is the opening and closing of the Strait. It is tempting to buy oil on the headlines, but digging down into who benefits from restricted LNG shipments and who has the fertilizer might be the better bets.