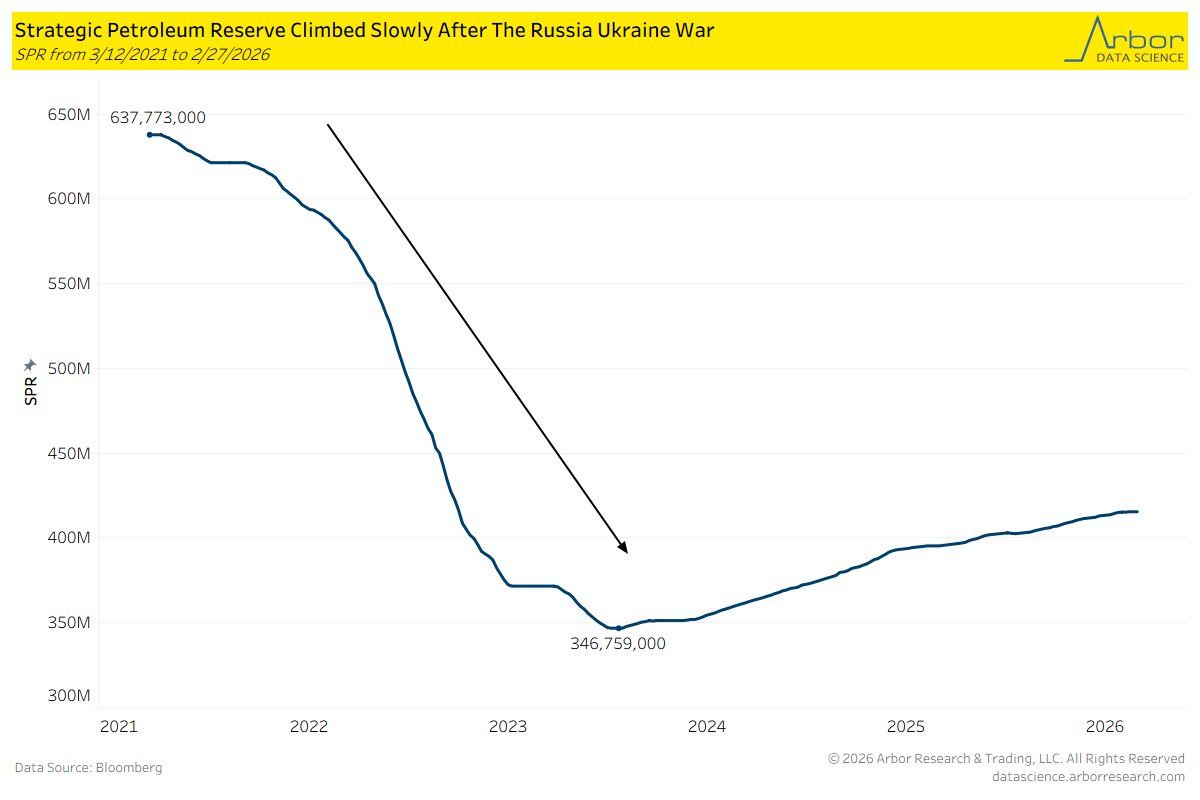

The U.S. has made consistent progress in rebuilding the Strategic Petroleum Reserve (SPR) following shocks from the Russia-Ukraine War. As of February 27, 2026, stockpiles had recovered to 415,441,000 barrels.

As of 3/6/2026, President Trump does not plan on tapping into the SPR.

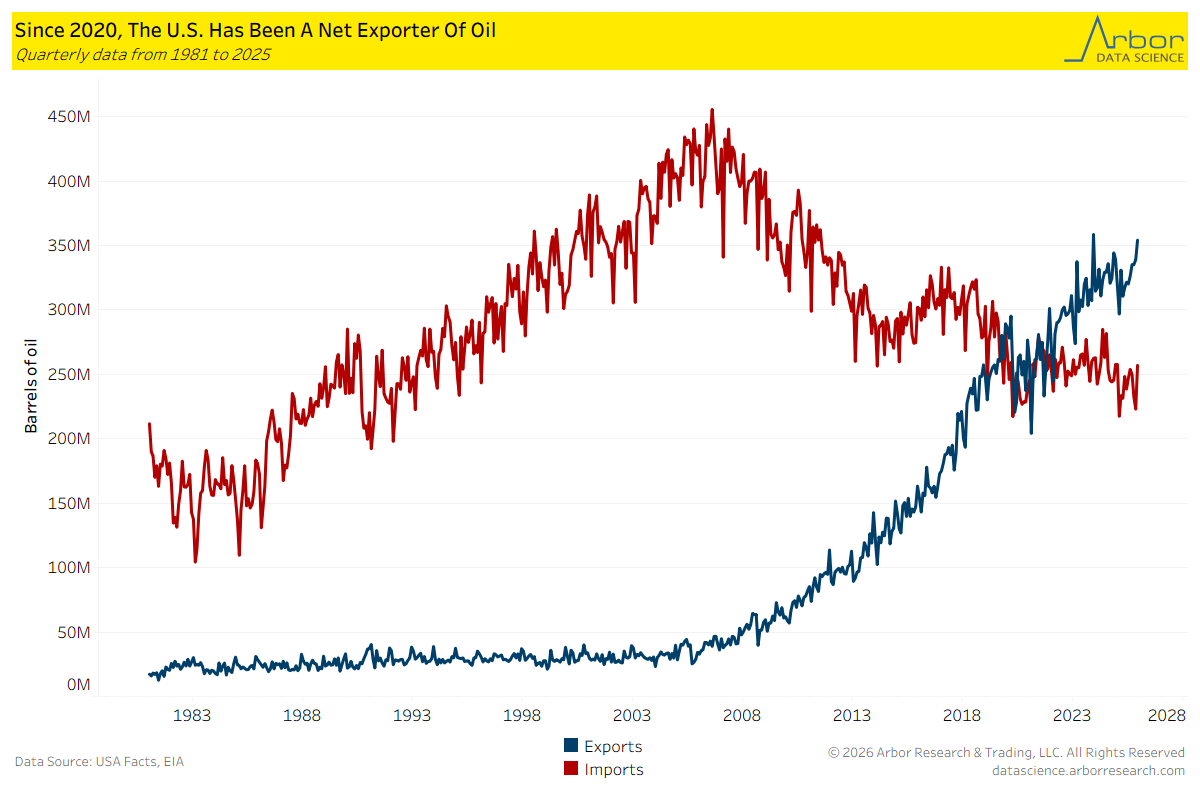

The U.S. has slowly shifted to becoming a net exporter of oil. From 2020 to 2025, the U.S. had exported more barrels of oil than it imported, a sign of strong domestic supply.

Given the volatility in the Strait of Hormuz, the U.S. should be able to remain resilient to these supply shocks, at least theoretically.

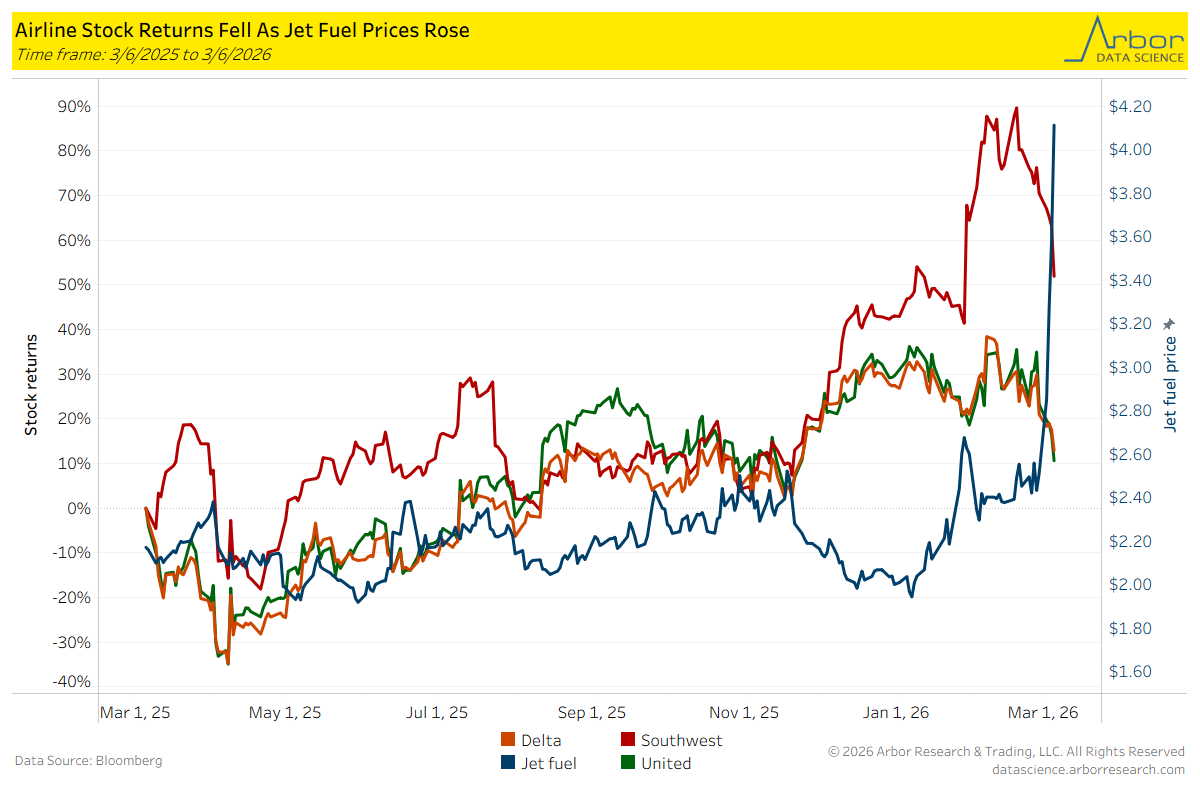

However, rising oil prices may continue to hurt U.S. businesses. One sector that is particularly sensitive to these shocks is the airline industry.

Although Delta, Southwest, and United all posted strong one-year performances, the surge in jet fuel prices — closely linked to oil prices — has eroded these gains. One-month performance for all three airlines was negative, hovering between -14% and -18%.

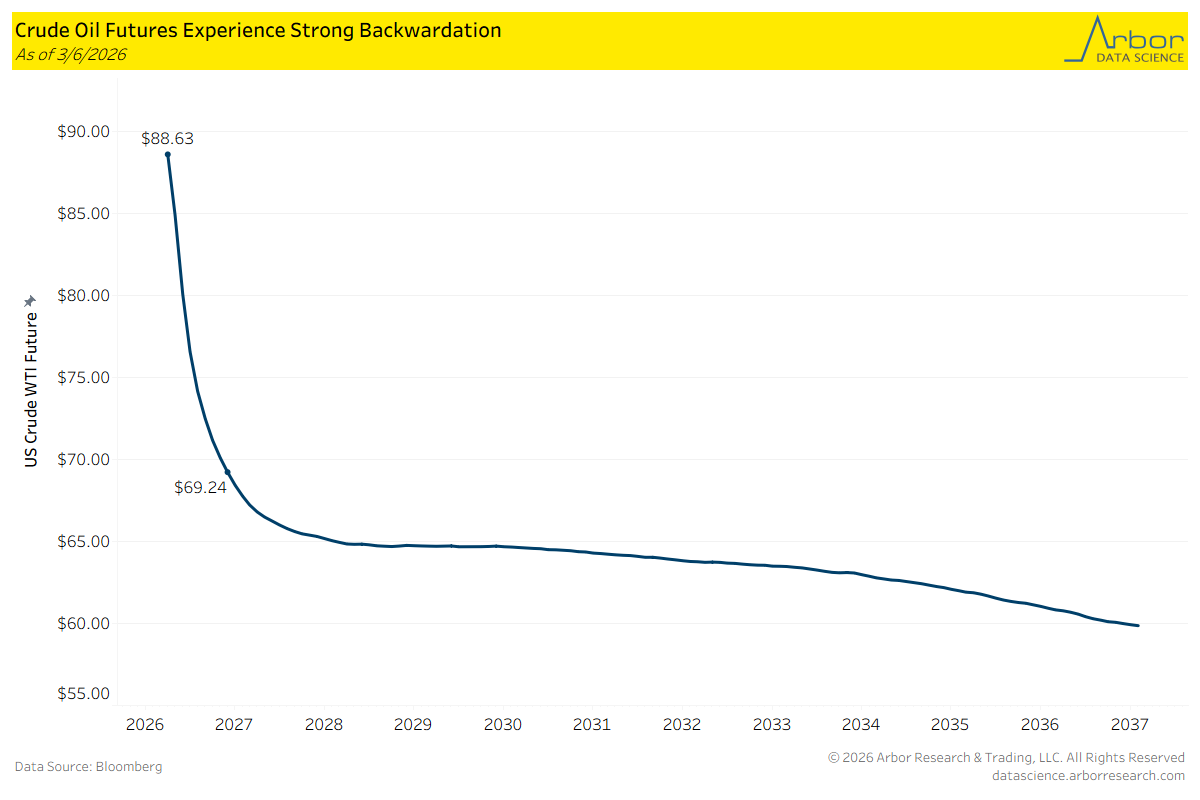

Strong backwardation in WTI crude oil futures indicates that traders believe the scarcity in oil supply will be short-lived. The spread between the April contracts and December contracts was nearly $20.

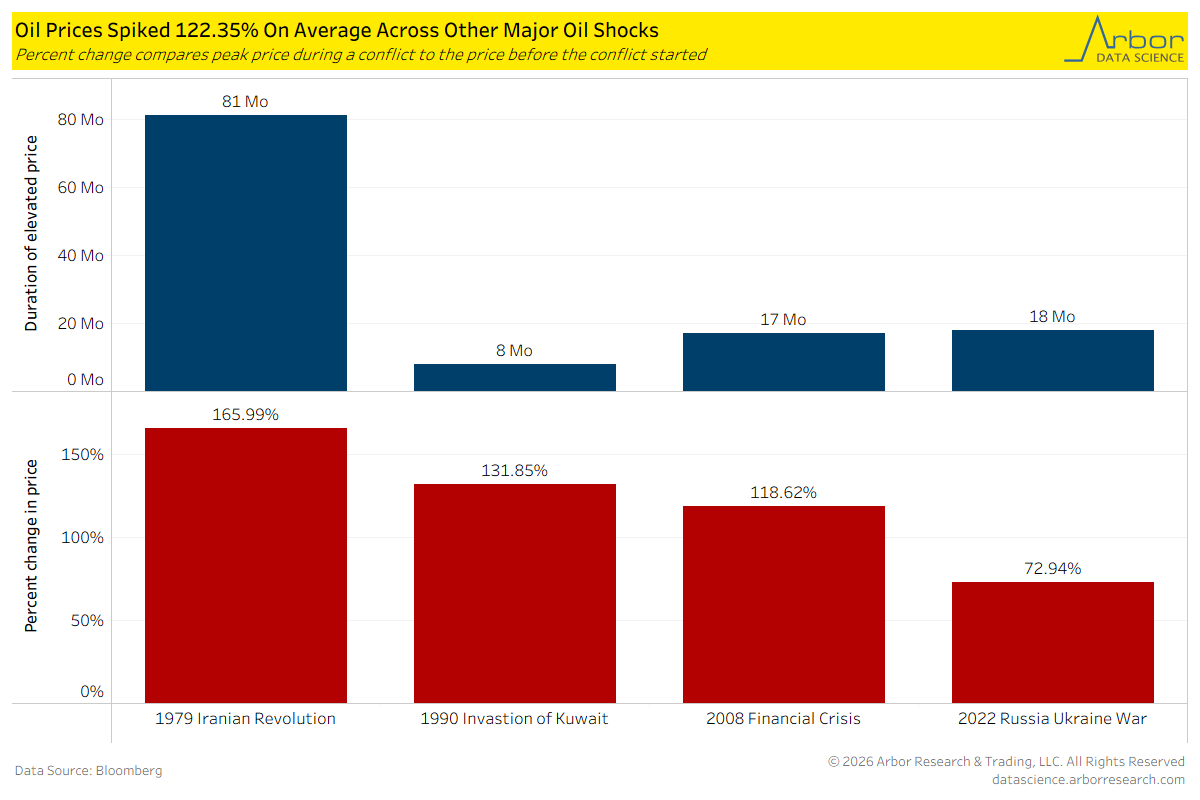

Looking at previous oil shocks, the average percentage increase in oil prices from before the crisis to the peak price was 122.35% across four major crises. The average duration of elevated prices, measured as the time it took to return to pre-crisis levels, was 31 months.

Only time will tell how the Iran conflict compares to these past shocks.