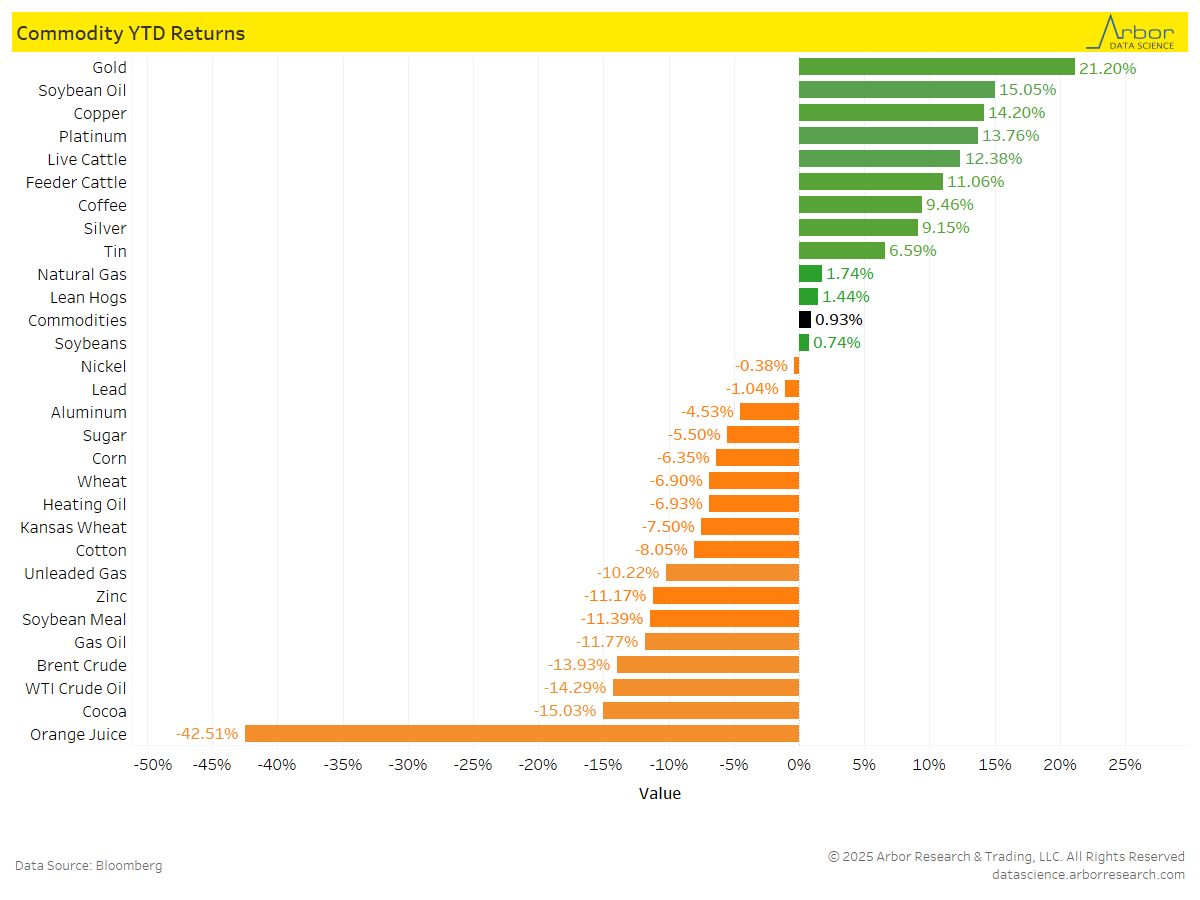

- Bloomberg’s Commodity Index, which is calculated on an excess return basis and reflects commodity futures price movements, was up 0.93% on a year-to-date (YTD) basis as of 5/30/25.

- YTD returns for commodities are shown in the chart below. Gold had the highest YTD return at 21.20%, followed by Soybean Oil at 15.05% and Copper at 14.20%.

- Orange Juice had the largest decrease, with a YTD return of -42.51%, followed by Cocoa at -15.03%.

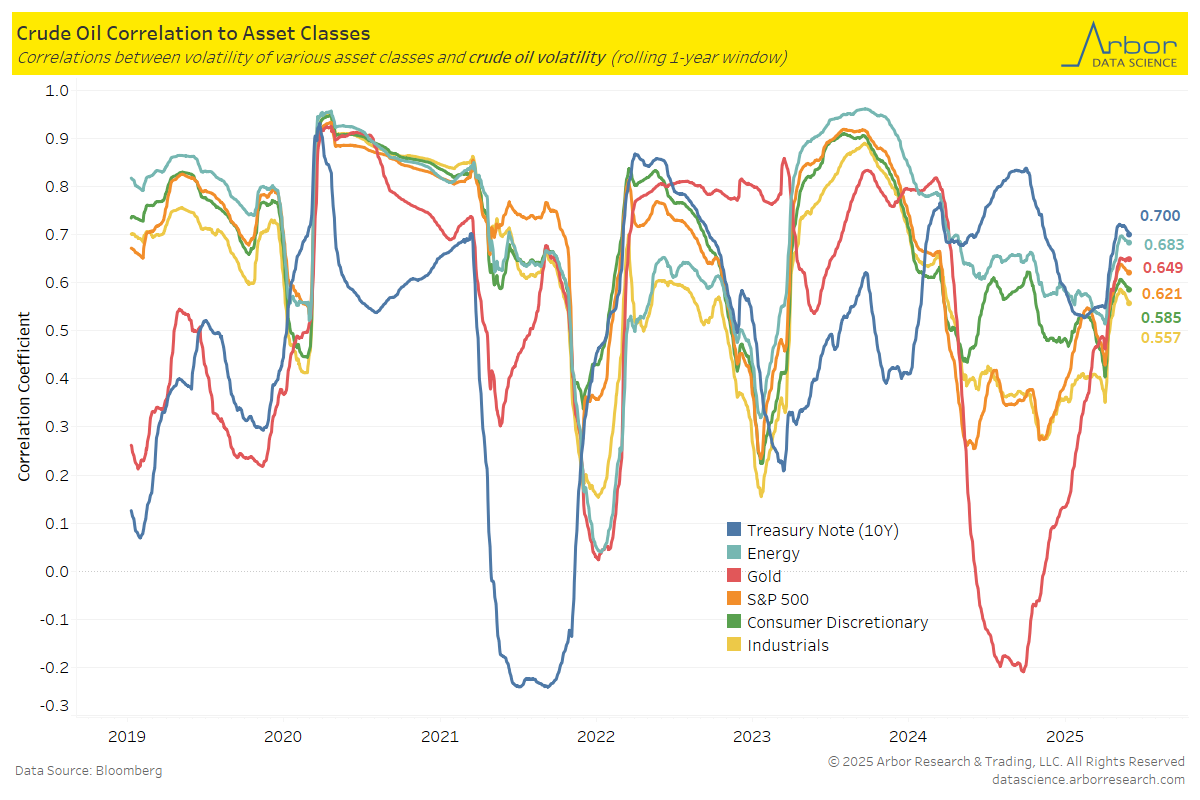

- The chart below illustrates the correlations between volatility of crude oil and volatility of various asset classes.

- As of 5/29/25, the 10-year Treasury Note volatility is the most correlated to crude oil volatility, with a correlation coefficient of 0.700.

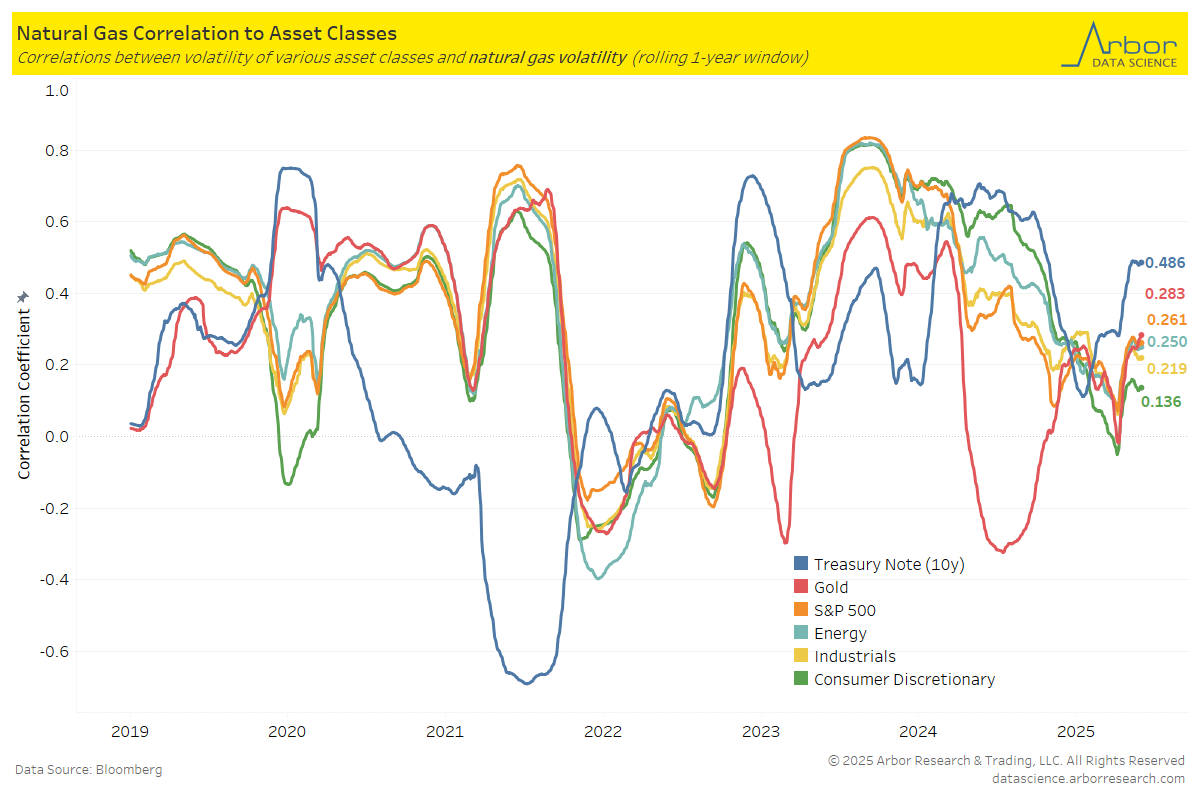

- The next chart outlines the correlations between the volatility of natural gas and the volatility of various asset classes.

- As of 5/29/25, the 10-year Treasury Note volatility is the most correlated to natural gas volatility, with a correlation coefficient of 0.486.

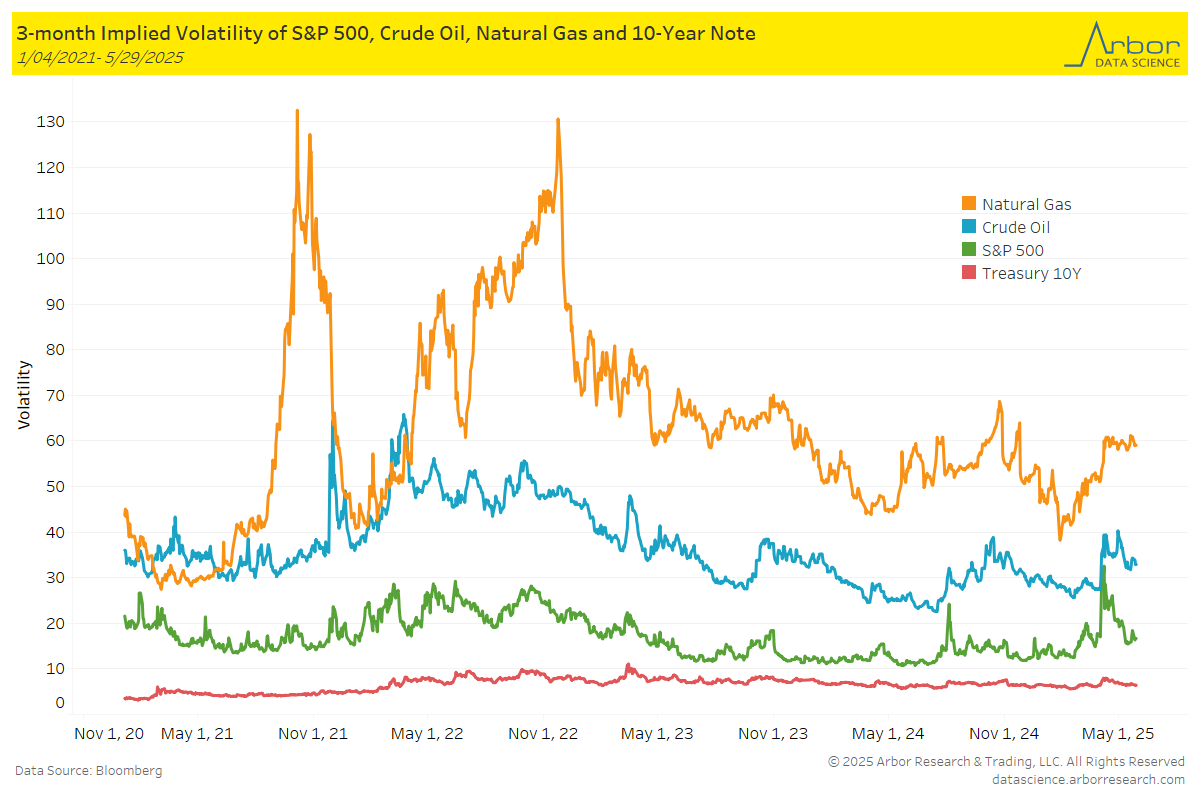

- The chart below highlights the 3-month implied volatility of the S&P 500, crude oil, natural gas, and the 10-Year Note as of 5/29/25.

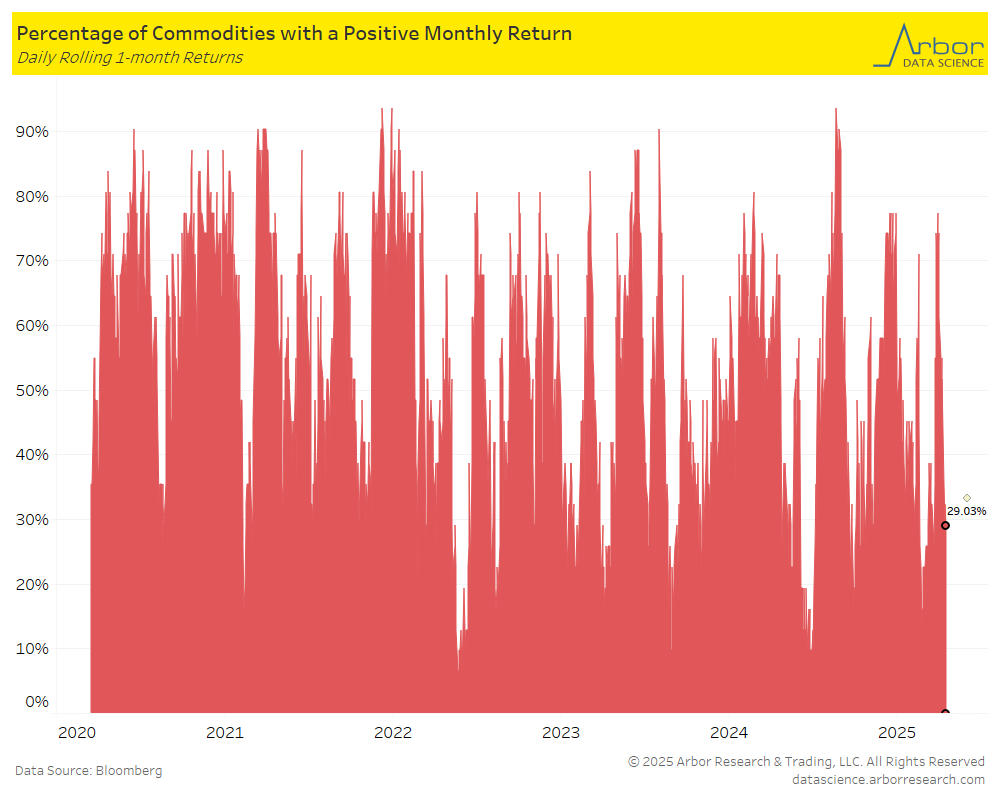

- The percentage of all commodities with a positive monthly return decreased to 29.03% on 5/29/25 from 45.16% the previous week (5/19/25-5/23/25).

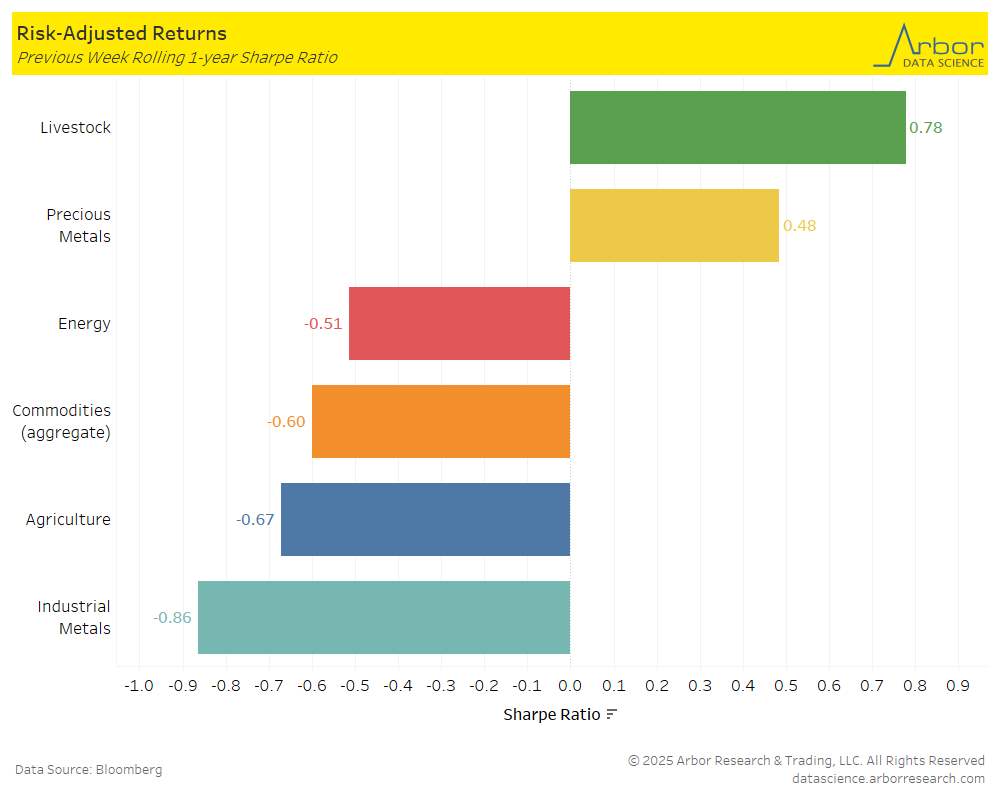

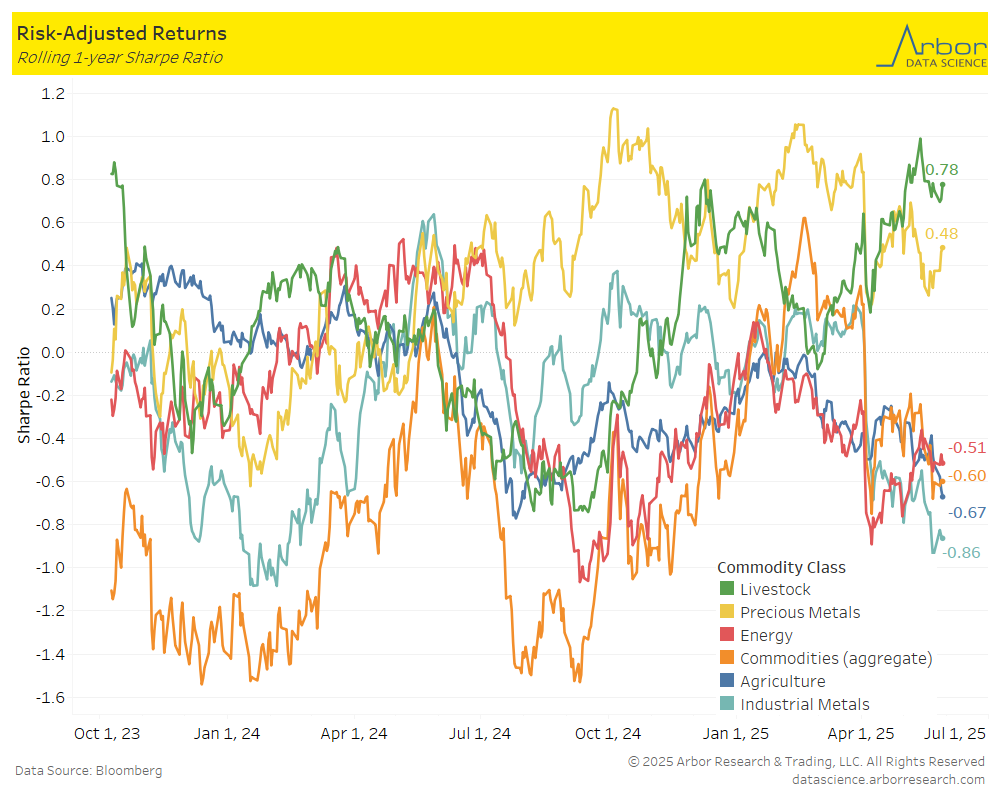

- The first chart below outlines the week-over-week (5/26/25-5/30/25) aggregate Sharpe ratio for commodities. It was -0.60 compared to -0.68 the prior week. The second chart is a rolling 1-year aggregate Sharpe ratio for commodities.

- Performance mostly increased week-over-week for the asset classes shown in the chart below The largest increase was in Precious Metals at 0.48 from 0.30 last week. The only decrease was in Agriculture at -0.67 from -0.48 the prior week.