We originally published this article on March 18, 2026. We are running it again as more clients and the mainstream media have now picked up on it.

In addition, our latest Arbor Data Science Podcast, published on March 20, 2026, featured Petr Pinkhasov discussing the critical role of helium in semiconductor manufacturing and the potential supply chain risks associated with it.

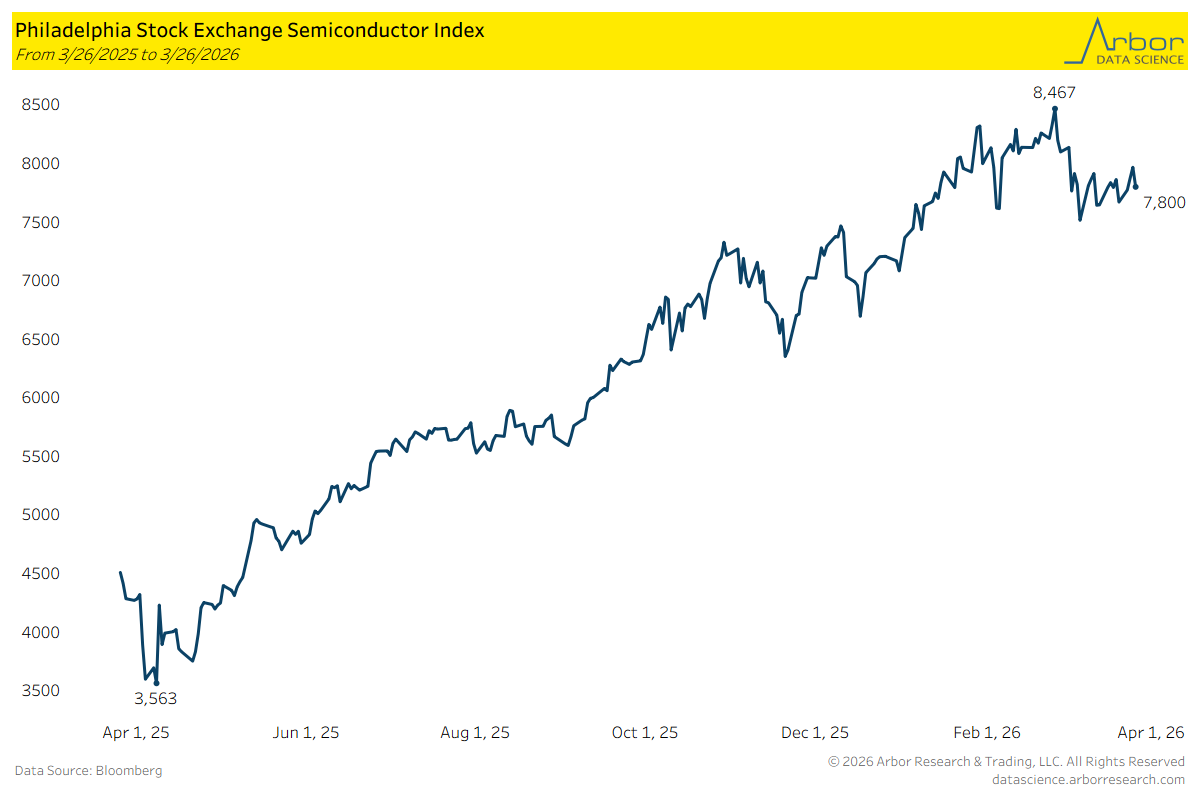

Semiconductors are still the market’s favorite trade, but the cracks are getting harder to ignore. The SOX rallied 120% off its April 2025 lows to an all-time high of 8,467 in February—then sold off 7% in two weeks as the Iran conflict exposed something the bulls hadn’t priced in: the physical supply chain that keeps this industry running passes through the Middle East.

Qatar’s Ras Laffan LNG complex got hit by an Iranian drone strike, taking roughly a third of global helium production offline. Helium has no substitute in chip manufacturing—it’s used in lithography cooling and wafer processing. No helium, no chips.

Containers already filled before the war are stranded behind a closed Strait of Hormuz. If the disruption extends beyond a few weeks, chipmakers will be forced to prioritize high-margin AI memory over everything else, deepening the shortage in consumer-grade DRAM and NAND that’s already been building for months.

Meanwhile, the broader numbers still look strong on paper. Global chip sales hit $792 billion in 2025, up 25.6%. Projections for 2026 are $975 billion to $1 trillion. Bank of America is calling it a supercycle. Memory prices have tripled in some configurations—DDR5 modules that were $250 in October are $700 now. Samsung just pushed back its Taylor, Texas fab to 2027. SK Hynix and Samsung have lost over $200 billion in combined market cap since the strikes.

The question isn’t whether semis are a secular growth story. The question is whether the market has priced in perfection at a time when the physical inputs to make these chips are under real threat.

This chart is the one that should worry the bulls. Semiconductor import prices peaked at 107.10 in late 2022 during the post-COVID shortage, then spent two years declining as supply chains normalized and inventory corrections played out. The index dropped all the way back to 99.50—below the 2012 baseline.

That means semiconductor import prices are now cheaper than they were 14 years ago in nominal terms. In real terms, adjusted for inflation, chips are dramatically cheaper. This is the deflationary force that has defined the industry for decades—Moore’s Law compressing the cost per transistor cycle after cycle. The 2021-2022 spike was the anomaly, driven by COVID supply chain chaos, not a structural shift.

Here’s why this matters now: the SOX is priced for a supercycle, but import prices are telling you the pricing power is gone. Yes, AI memory and HBM are commanding premium prices. But those are a fraction of total chip volume—20 million units out of 1.05 trillion chips sold. The other 99.998% of chips are seeing prices normalize or decline. When the index that tracks what the U.S. actually pays for imported semiconductors is back to 2012 levels, the idea that the entire sector deserves peak-cycle multiples is a stretch.

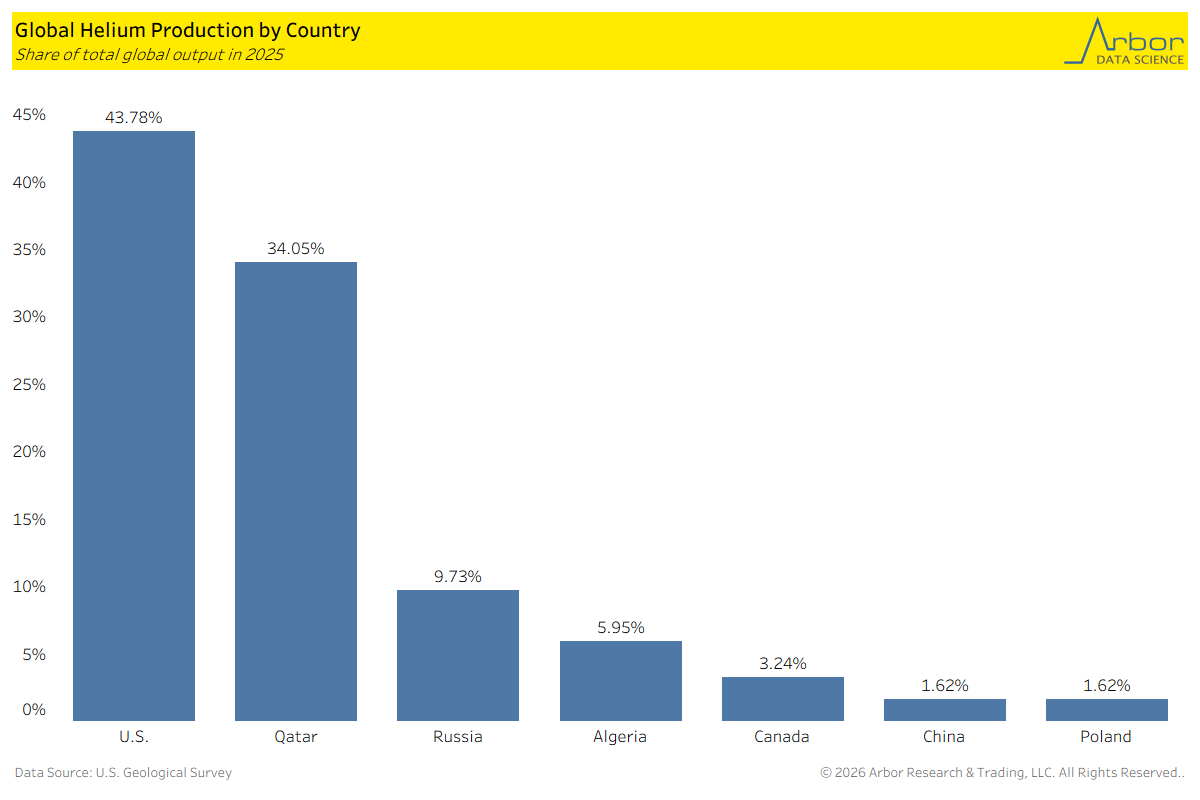

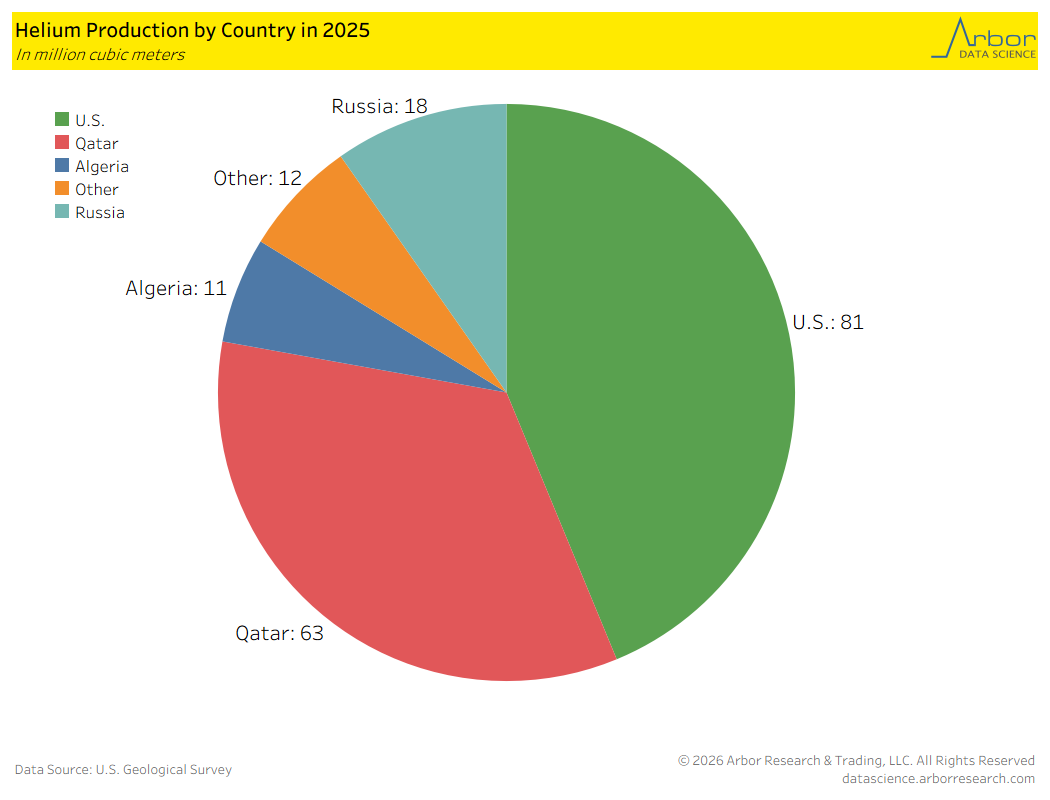

The U.S. produces 43.78% of the world’s helium. Qatar produces 34.05%. Together, that’s nearly 78% of global supply concentrated in two countries. Russia is a distant third at 9.73%, followed by Algeria at 5.95%.

The Iran conflict just took Qatar’s share offline. Ras Laffan produces helium as a byproduct of LNG processing—when LNG production stops, helium production stops. There’s no way to isolate one from the other. And unlike oil, there’s no strategic helium reserve to draw from. No OPEC+ to add barrels. No spare capacity sitting idle. The U.S. can’t ramp its 44% share fast enough to cover a 34% hole. This is a genuine supply shock in a market that was already described as the tightest in years before a single missile hit Qatar.

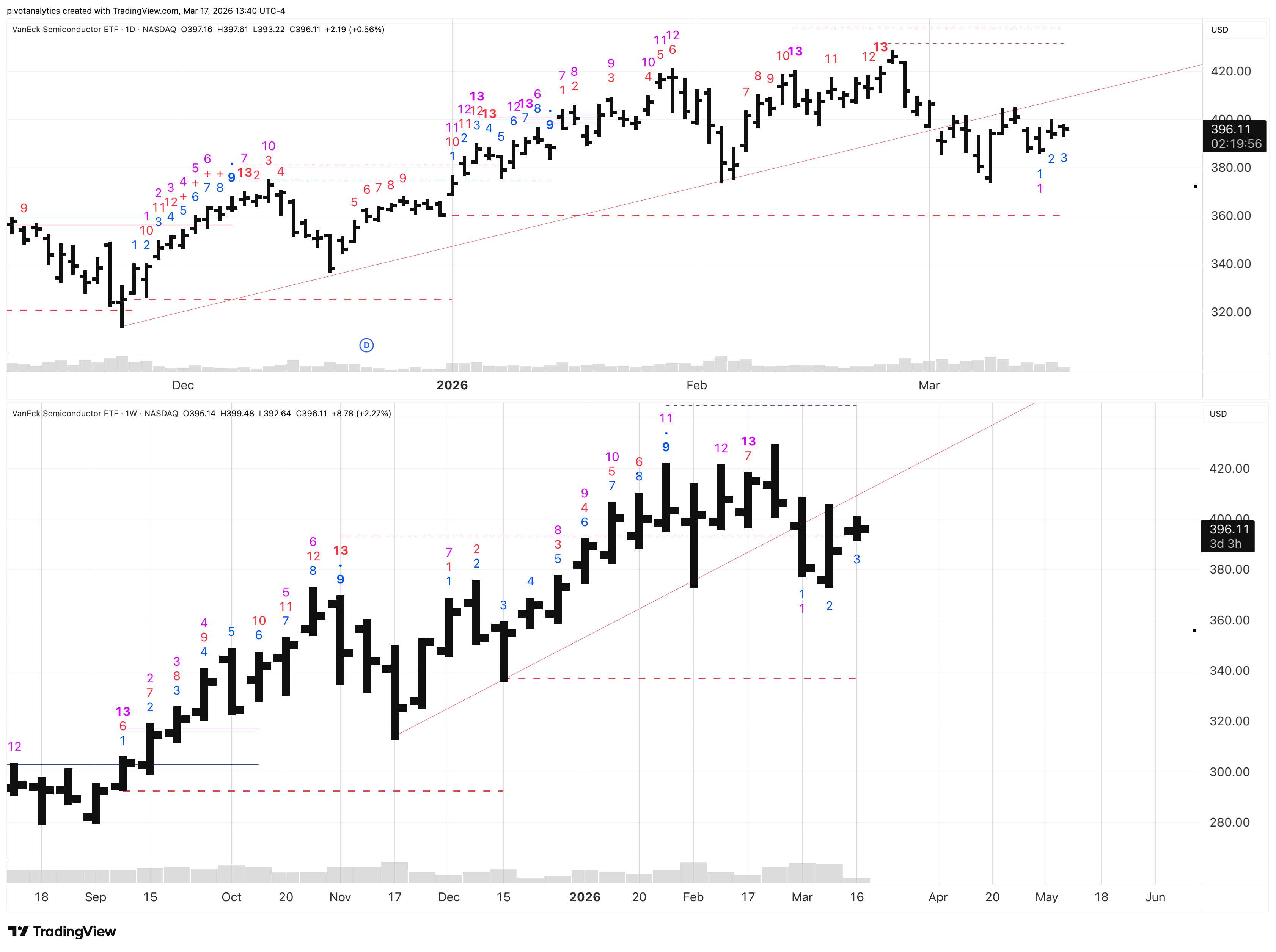

On the technicals, my position has gotten stronger since the last update. I’ve been pointing out the DeMark exhaustion at the highs on SMH (Semiconductor ETF) and since then the sector has broken down a clear trend which we retested and failed to hold above so far. I’m still in the position given the cracks in private credit, financial conditions getting worse and this being a very frothy part of the market, this is technically very vulnerable here.