Our last update on the AI theme covered data centers. They are hyperscalers dumping $350-400 billion into AI infrastructure, with construction up 23% while, every other category was contracting. But, all of that spending has to go somewhere. And a huge chunk of it flows directly into semiconductors.

Bank of America is calling this a “supercycle similar to the boom of the 1990s.” The industry did $772 billion in sales in 2025—up 22.5%—and it is projected to hit $975 billion to $1 trillion in 2026. AI is the driver. Memory demand is through the roof, and chipmakers are responding with price hikes across the board. Texas Instruments raised prices 10-30% on over 60,000 models. Analog Devices just bumped prices 15% across the board, with military-grade parts up 30%. Memory prices are expected to climb another 40% through Q2 2026. Hence, this is why Micron is on absolute fire right now. Not sure how much better it can get for them.

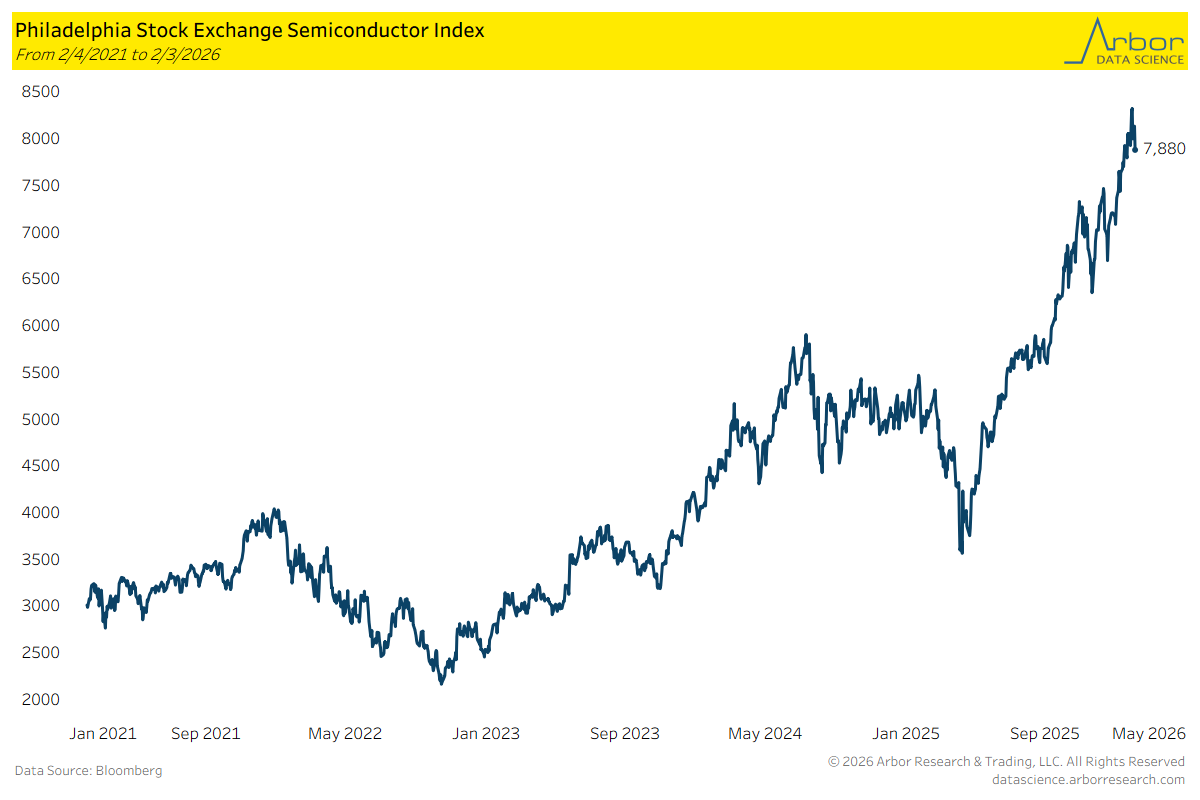

The SOX index bottomed around 2,200 in late 2022 when the Fed was hiking and everyone thought tech was dead. Since then? A relentless climb to 7,880—nearly 4x off the lows in just over three years. The VanEck Semiconductor ETF rallied 49% in 2025, its third straight winning year. 2023 was even crazier at 72%. Rate hikes, recession fears, China export controls—AI demand steamrolled all of it.

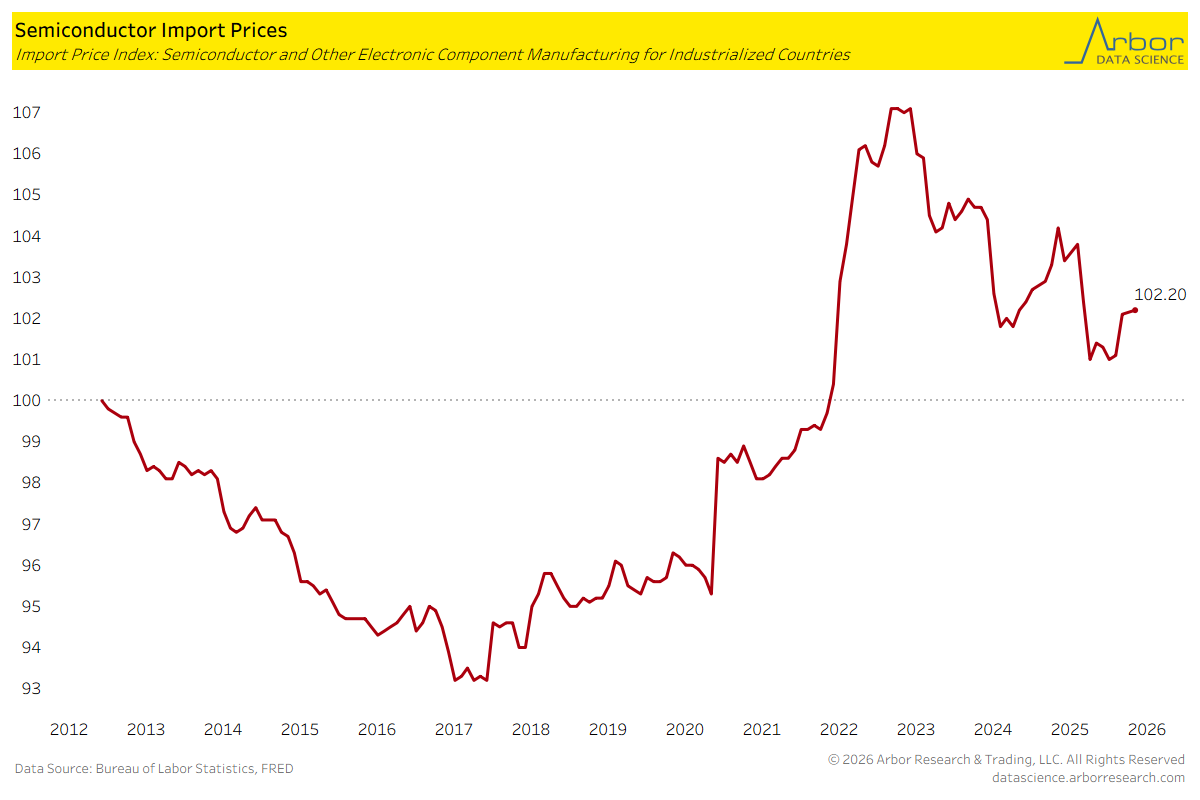

Semiconductor import prices spiked to 107 during the COVID supply crunch, then normalized down to around 101 by mid-2025. Now they’re ticking back up to 102.20. The difference this time around is that it’s not supply chain chaos—it’s demand. AI chips, HBM memory, and advanced packaging are all capacity-constrained. Foundries are raising prices because they can. TSMC, Samsung, and the memory giants have pricing power they haven’t had in years.

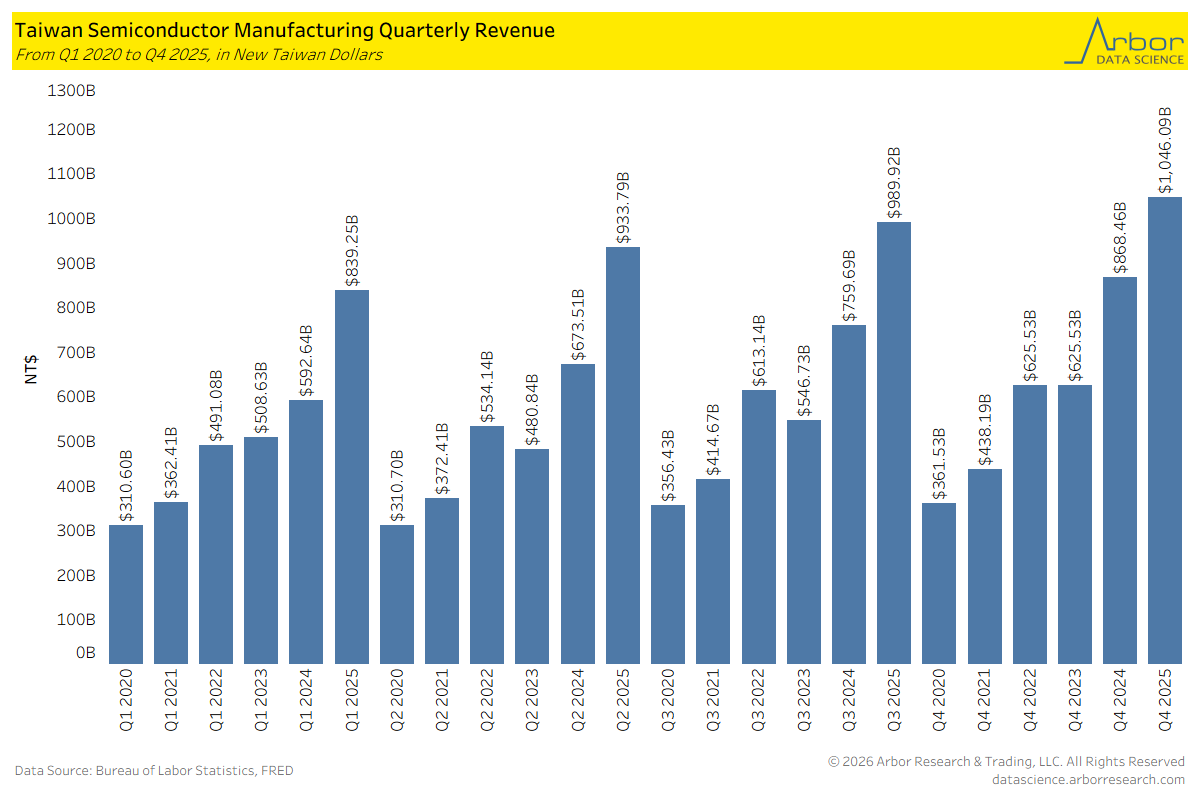

TSMC just printed NT$1.046 trillion in Q4 2025—a record quarter and the first time they’ve cracked a trillion in New Taiwan Dollars. For context, they were doing NT$310 billion quarters back in 2020. This is the AI buildout showing up in real numbers. TSMC makes the chips that power Nvidia’s GPUs, Apple’s processors, and AMD’s data center products. When hyperscalers spend $400 billion on data centers, a massive chunk flows straight to TSMC.

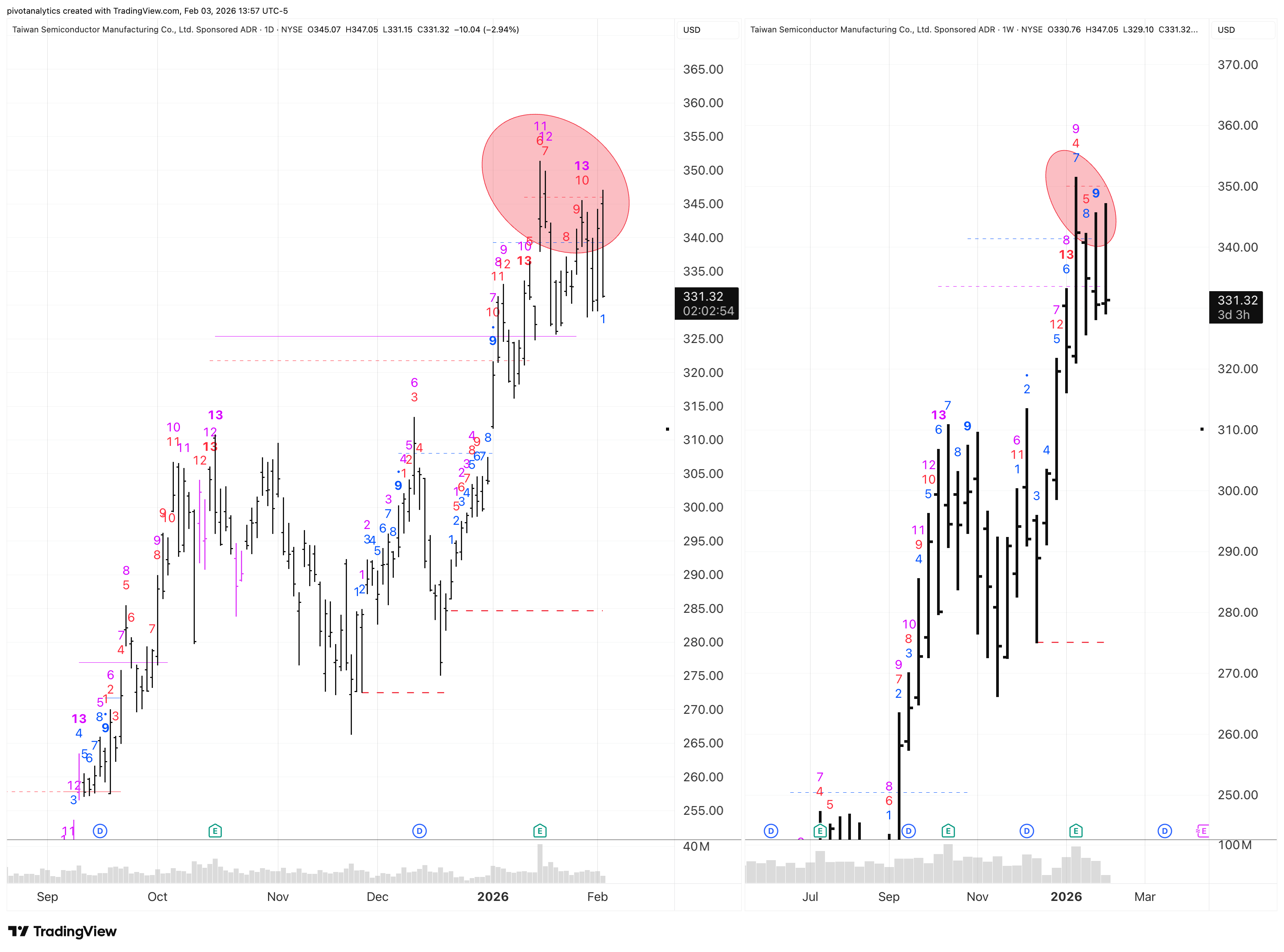

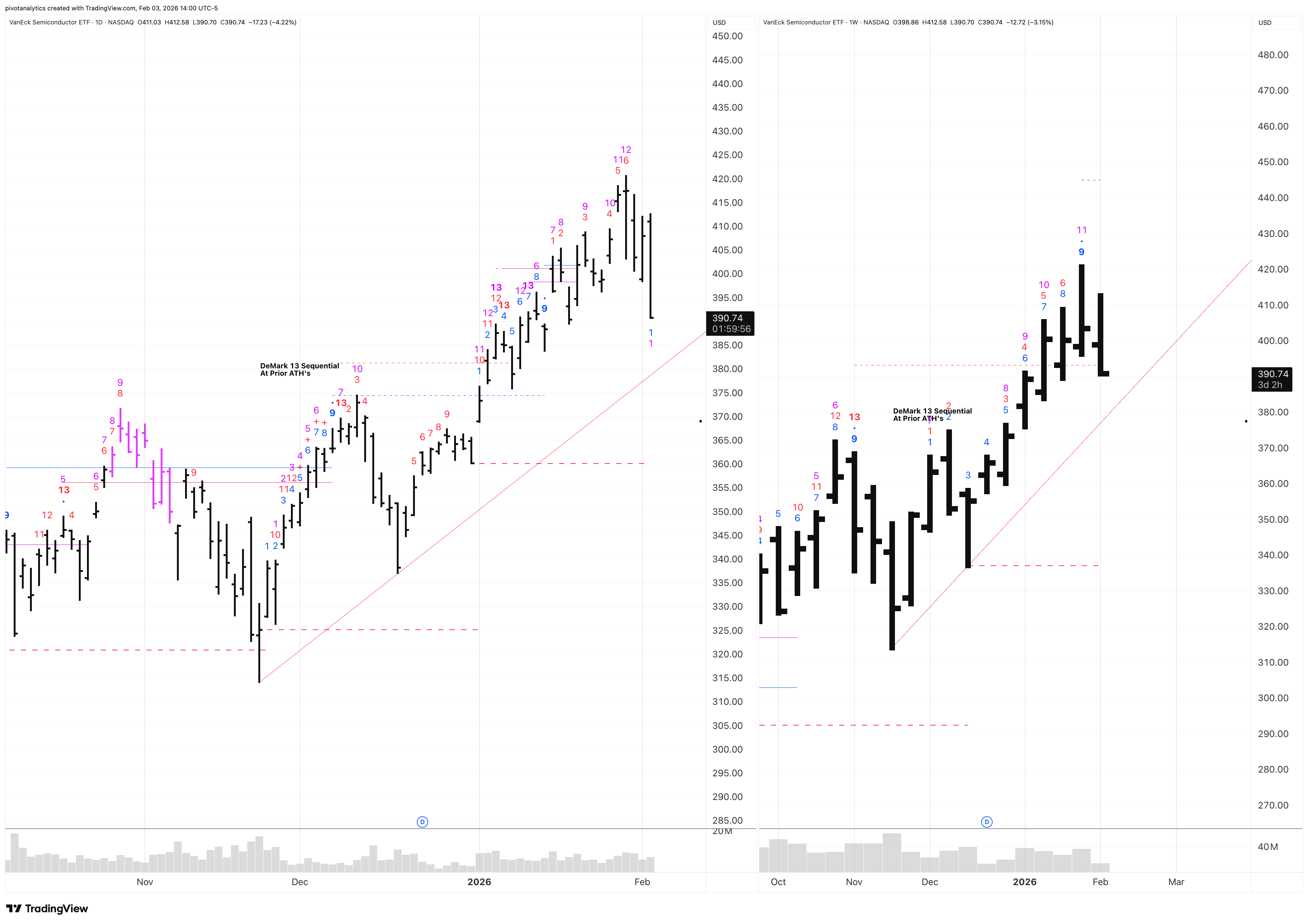

On the technical side, I’m still seeing a moderate uptrend in the semis, but the rest of the indices and single names are showing exhaustion and potential weakness. I’ve been beating a dead horse on bear thesis for semiconductors so I won’t bore you all with it again, but all of the good things are very much priced in at this point. I’m looking for a buy point on the semi conductors, but not here yet. I’m looking at 340 on the weekly charts as an important zone on SMH.

Taiwan semi completed weekly 9 sell setups and daily 13 combos recently, so I’m not looking to be a buyer up here.